2019: Issue 712, Week: 02nd - 06th December

A Weekly Update from SMC (For private circulation only)

WISE M NEY

NEY

2019: Issue 712, Week: 02nd - 06th December

A Weekly Update from SMC (For private circulation only)

NEY

![]() Customized Plans

Customized Plans

![]() Comprehensive Investment Solutions

Comprehensive Investment Solutions

![]() Long-term Focus

Long-term Focus

![]() Independent & Objective Advise

Independent & Objective Advise

![]() Financial Planning

Financial Planning

Call Toll-Free 180011 0909

Visit www.smcindiaonline.com

| Equity | 4-7 |

| Derivatives | 8-9 |

| Commodity | 10-13 |

| Currency | 14 |

| IPO | 15 |

| FD Monitor | 16 |

| Mutual Fund | 17-18 |

I

n the week gone by, in the first part of the week global markets rallied near-record highs, after data showed U.S. economic growth had picked up in the third quarter and consumer spending had increased. However, they got stalled on Thursday after China said it would retaliate for U.S. legislation backing Hong Kong's protesters, leaving investors concerned as to the extent of the Chinese response. Waning hopes of reconciliation between the world's two biggest economies before additional, possibly damaging tariff hikes also left the investor in dilemma. Meanwhile, Japanese retail figures slumped the most since 2015 as a sales tax hike hauled on the economy, intensifying a slowdown caused by slowing exports and manufacturing.

Back at home, on Friday equity markets declined from their record high ahead of quarterly GDP growth data release and amid discouraging cues from global peers. Investors feared that the passage of the Hong Kong pro-democracy bill in Washington could derail trade talks between the United States and China. However in the first part of the week market continue to rally up on consistent buying by the foreign institutional investors. Undoubtedly, foreign funds have bought big in India this month thus, pushing the market to higher levels. However, the recent data showed that India’s gross domestic product (GDP) grew 4.5 percent in July-September 2019, the lowest since the fourth quarter of 2012-13, confirming fears of a deepening slowdown in the economy. The slowdown comes on the back of the 5 percent GDP growth recorded in April-June and 7.1 percent in July-September last year. Upcoming macroeconomic data and global cues will continue to give direction to the markets.

On the commodity market front, uncertainty regarding US China trade deal is keeping the bullion counter in tight range as US nonfarm payroll data this week will give further direction to the prices. December being a crucial month we will be getting more clarity on the tentative meeting that will be held between US and China and UK elections that is scheduled on 12th December. Crude oil prices may remain on sideways path as participants have now shifted their focus on this week’s meeting on 5th and 6th December as OPEC and allies including Russia, a group known as OPEC+, which have been withholding production to support prices. It is expected that OPEC+ to roll over its current production-cut deal, which is set to expire at the end of March 2020 , by three to six months. The downside pressure can persist in natural gas counter amid warmer weather forecasts. This week US ISM manufacturing and non manufacturing PMI, jobless claim data, US export and imports data and nonfarm payroll data, US factory orders and China manufacturing PMI are some very important triggers for this week.

SMC Global Securities Ltd. (hereinafter referred to as “SMC”) is a registered Member of National Stock Exchange of India Limited, Bombay Stock Exchange Limited and its associate is member of MCX stock Exchange Limited. It is also registered as a Depository Participant with CDSL and NSDL. Its associates merchant banker and Portfolio Manager are registered with SEBI and NBFC registered with RBI. It also has registration with AMFI as a Mutual Fund Distributor.

SMC is a SEBI registered Research Analyst having registration number INH100001849. SMC or its associates has not been debarred/ suspended by SEBI or any other regulatory authority for accessing /dealing in securities market.

SMC or its associates including its relatives/analyst do not hold any financial interest/beneficial ownership of more than 1% in the company covered by Analyst. SMC or its associates and relatives does not have any material conflict of interest. SMC or its associates/analyst has not received any compensation from the company covered by Analyst during the past twelve months. The subject company has not been a client of SMC during the past twelve months. SMC or its associates has not received any compensation or other benefits from the company covered by analyst or third party in connection with the research report. The Analyst has not served as an officer, director or employee of company covered by Analyst and SMC has not been engaged in market making activity of the company covered by Analyst.

The views expressed are based solely on information available publicly available/internal data/ other reliable sources believed to be true.

SMC does not represent/ provide any warranty express or implied to the accuracy, contents or views expressed herein and investors are advised to independently evaluate the market conditions/risks involved before making any investment decision.

DOMESTIC NEWS

Automobile

• A shok Leyland has bagged an order from Tamil Nadu State Transport Undertakings (TNSTU) for 1,750 buses. The order comes close on the back of orders received from various state transport undertakings.

• Bajaj Auto has joined hands with YULU, the largest shared e-mobility service provider, to transform urban commute in India. Bajaj Auto is investing $8mn in YULU , to compliment this strategic relationship. YULU will source from Bajaj electric two-wheelers which have been co-designed and manufactured exclusively for shared micro-mobility. Bajaj will also consider facilitating the vehicle finance needs of YULU for a large scale deployment of its micro-mobility electric vehicles.

Pharmaceuticals

• Aurobindo Pharma announced that Auro Vaccines LLC, 100% subsidiary of Aurobindo Pharma USA Inc., which in turn is 100% subsidiary of the Company, has entered into a definitive agreement to acquire certain business assets from Profectus BioSciences Inc., USA., a clinical-stage vaccine development company.

• Cipla announced that its wholly owned subsidiary, Cipla (EU), holding 60% stake in Cipla Pharma Lanka, Sri Lanka, has signed an agreement with CitiHealth Imports to acquire the remaining 40% stake in Cipla Pharma Lanka. Post acquisition, Cipla Lanka will become a wholly owned subsidiary.

• Alembic Pharmaceuticals announced that the Company has received final approval from the US Food & Drug Administration (USFDA) for its Abbreviated New Drug Application (ANDA) Silodosin Capsules, 4 mg and 8 mg. The approved ANDA is therapeutically equivalent to the reference listed drug product (RLD), Rapaflo Capsules, 4 mg and 8 mg, of Allergan Sales, LLC. Silodosin capsule, a selective alpha-1 adrenergic receptor antagonist, is indicated for the treatment of the signs and symptoms of benign prostatic hyperplasia (BPH).

Hotel

• Lemon Tree Hotels has launched a 101 Rooms hotel — 'Red Fox Hotel' in Vijayawada. Set on the banks of the Krishna River in the city of Vijayawada, it is an ideal destination for both business and leisure travellers. Just 15 kms from the railway station, it is in close proximity to the ornate Kanaka Durga Temple, nestled on the Indrakeeladri Hill, the Undavalli Caves featuring ancient rock—cut temples and the Bhavani Island on the Krishna River.

Engineering

• Ashoka Buildcon has received Letter of Award (LOA) from Uttar Pradesh Expressways Industrial Development Authority (UPEIDA) in respect of the Project viz. Development of Bundelkhand Expressway Project (PackageIII): From Kaohari (Dist. Mahoba) to BaroliKharka (Dist. Hamirpur) (Km 100+000 to Km 149+000) in the State of Uttar Pradesh on EPC Basis.

FMCG

• Godrej Consumer Products has introduced Godrej aer smart matic air fresheners, India's first mobile controlled smart home fragrance. The product will be available in two fragrances at MRP of Rs 799 on www.godrejaer.com and very soon on ecommerce and modern retail chains.

Chemicals

• BASF India announced that the company plans to double its capacity for polymer dispersions with a new production line at its site in Dahej, Gujarat. Through this investment, the Company aims to provide a reliable supply of high-quality dispersion solutions to customers in the fast-growing Indian and South Asian markets.

INTERNATIONAL NEWS

• US real gross domestic product jumped by 2.1 percent in the third quarter compared to the previously estimated 1.9 percent increase. Economists had expected the pace of GDP growth to be unrevised.

• US pending home sales index plunged by 1.7 percent to 106.7 in October after surging up by 1.4 percent to a revised 108.6 in September. Economists had expected pending home sales to climb by 0.8 percent compared to the 1.5 percent jump originally reported for the previous month.

• US durable goods orders climbed by 0.6 percent in October after plunging by a revised 1.4 percent in September. Economists had expected durable goods orders to decrease by 0.8 percent compared to the 1.2 percent slump that had been reported for the previous month.

• US initial jobless claims dropped to 213,000, a decrease of 15,000 from the previous week's revised level of 228,000. Economists had expected jobless claims to dip to 221,000 from the 227,000 originally reported for the previous week.

• US new home sales fell by 0.7 percent to an annual rate of 733,000 in October after surging up by 4.5 percent to an upwardly revised rate of 738,000 in September. Economists had expected new home sales to jump by 1.1 percent to a rate of 709,000 from the 701,000 originally reported for the previous month.

• China's industrial profits declined at a faster pace in October largely due to falling producer prices and slowdown in production and sales growth. Industrial profits decreased 9.9 percent on a yearly basis in October, following a 5.3 percent decrease in September. This was the third consecutive decrease.

| Stocks | *Closing Price | Trend | Date Trend Changed | Rate Trend Changed | SUPPORT | RESISTANCE | Closing S/l |

|---|---|---|---|---|---|---|---|

| S&P BSE SENSEX | 40794 | UP | 08.02.19 | 36546 | 36300 | 35300 | |

| NIFTY50 | 12056 | UP | 08.02.19 | 10944 | 10900 | 10600 | |

| NIFTY IT* | 14998 | UP | 21.07.17 | 10712 | - | 14800 | |

| NIFTY BANK | 31946 | UP | 30.11.18 | 26863 | 27700 | 27000 | |

| ACC | 1522 | DOWN | 04.10.19 | 1488 | 1540 | 1565 | |

| BHARTIAIRTEL | 442 | UP | 15.03.19 | 338 | 410 | 390 | |

| BPCL | 512 | UP | 30.08.19 | 355 | 470 | 450 | |

| CIPLA | 467 | UP | 25.10.19 | 460 | 440 | 430 | |

| SBIN | 342 | UP | 01.11.19 | 314 | 315 | 305 | |

| HINDALCO** | 200 | DOWN | 15.11.19 | 188 | - | 203 | |

| ICICI BANK | 513 | UP | 20.09.19 | 418 | 480 | 470 | INFOSYS | 696 | DOWN | 25.10.19 | 637 | 690 | 720 |

| ITC | 246 | DOWN | 31.05.19 | 279 | 260 | 270 | |

| L&T | 1331 | DOWN | 15.11.19 | 1378 | 1410 | 1430 | |

| MARUTI | 7246 | DOWN | 06.12.19 | 6450 | 7100 | 6900 | |

| NTPC | 116 | DOWN | 16.08.19 | 118 | 126 | 130 | |

| ONGC | 132 | DOWN | 06.12.19 | 134 | 134 | 130 | |

| RELIANCE | 1551 | UP | 16.08.19 | 1278 | 1460 | 1440 | |

| TATASTEEL | 428 | UP | 01.11.19 | 396 | 390 | 375 | |

*NIFTYIT has broken support of 15200**Hindalco has breached the resistance of 198

Closing as on 06-12-2019

NOTES:

1) These levels should not be confused with the daily trend sheet, which is sent every morning by e-mail in the name of "Morning Mantra ".

2) Sometimes you will find the stop loss to be too far but if we change the stop loss once, we will find more strength coming into the stock. At the moment, the stop loss will be far as we are seeing the graphs on weekly basis and taking a long-term view and not a short-term view.

| Meeting Date | Company | Purpose |

|---|---|---|

| 3-Dec-19 | Redington (India) | Interim Dividend - Rs 1.50 Pr Sh |

| 4-Dec-19 | Manugraph India | Annual General Meeting/Dividend - Rs 0.50 Per Share |

| 5-Dec-19 | HCL Technologies | Bonus 1:1 |

| 5-Dec-19 | Bharat Road Network | Dividend - Rs 0.50 Per Share |

| 5-Dec-19 | HeidelbergCement India | Interim Dividend - Rs 1.50 Per Share |

| 5-Dec-19 | Thomas Cook (India) | Demerger |

| 10-Dec-19 | Nestle India | Interim Dividend |

| 13-Dec-19 | Trident | FV Split (Sub-Division) - From Rs 10/- To Rs 1/- Per Share |

| 18-Dec-19 | Borosil Glass Works | Dividend - Rs 0.65 Per Share |

| 26-Dec-19 | Balmer Lawrie & Company | Bonus 1:2 |

| Meeting Date | Company name | Purpose |

|---|---|---|

| 3-Dec-19 | Gufic Biosciences | Quarterly Results |

| 3-Dec-19 | Nestle India | Interim Dividend |

| 5-Dec-19 | Khaitan (India) | Quarterly Results |

| 6-Dec-19 | Centrum Capital | Quarterly Results |

| 7-Dec-19 | Unitech | Quarterly Results |

| 12-Dec-19 | Smartlink Holding | Quarterly Results |

4

5

Federal Bank Limited

CMP: 90.85

Target Price: 113

Upside: 25%

| Face Value (Rs.) | 2.00 |

| 52 Week High/Low | 110.35/78.40 |

| M.Cap (Rs. in Cr.) | 18088.03 |

| EPS (Rs.) | 7.85 |

| P/E Ratio (times) | 11.58 |

| P/B Ratio (times) | 1.29 |

| Stock Exchange | BSE |

Investment Rationale

• T he total business of the bank grew 17% Y-o-Y from Rs.255440 Cr as on September 2019 while the deposits growth was strong at 18% to Rs 139547 crore at end September 2019, Gross advances book increased 15% yoy to Rs 115893 crore at end September 2019. The corporate book grew at slow pace of 9% to Rs 60465 crore. The bank has improved the loan mix in favour of retail gaining share to 50% with balance accounting for corporate loan book. CASA increased 12% to Rs. 44023 Crore.

• It has reported 10% growth in Net Interest Income (NII) at Rs 1123.78 crore for the quarter ended September 2019. The interest earned rose 18% to Rs 3254.25 crore, while interest expended moved up 22% to Rs 2130.47 crore in the quarter ended September 2019.

• The Gross NPA and Net NPA of the Bank as at the end of the Quarter stood at Rs.3612.11 Cr and Rs. 1843.64 Cr respectively. Gross NPA as a percentage stood at 3.07% and Net NPA as a percentage stood at 1.59%.The Provision Coverage Ratio (including technical write-offs) is 66.16%.

• The bank maintained the guidance for RoA of 1.1% for FY2020 as reduction in the corporate tax rate provides upside. The bank aims to improve RoA to 1.25% in FY2021 and 1.5% in FY2022.

• The bank had guided at 4 stressed accounts at the beginning of the year with exposure of Rs 700 crore. The bank did not witness any new challenges on asset quality front in last six months, so bank has continued to maintain slippage guidance for FY2020. The bank has also maintained the credit cost guidance of 60 bps for Fy2020.

• The bank expects to improve provision coverage ratio to 70% by end March 2020.

• The management of the bank has guided 22-25%

loan growth during the year. NIM guidance is 3.10- 3.15% for March 2020 quarter.

The Bank has 1251 branches and 1942 ATMs at the end of September 2019.

Risk

• Strict Regulatory guidelines

• Liquidity risk

Valuation

The bank of the business grew strongly and management of the bank have focus in wholesale banking which would continue to give strong, balanced credit growth, improvement in asset quality. The bank has empanelled in 15 states and catering 200 government entities. New partnerships in General Insurance with Tata AIG and HDFC Ergo to augment fee income also has opened new Call Centre for Cross Selling products like Credit Card, Insurance and to extend exclusive support to Ultra HNI and NRE Customers would help to increase other income. Thus, it is expected that the stock will see a price target of Rs.113 in 8 to 10 months time frame on one year P/Bvx 1.40 and FY21 (BVPS) of Rs.80.95.

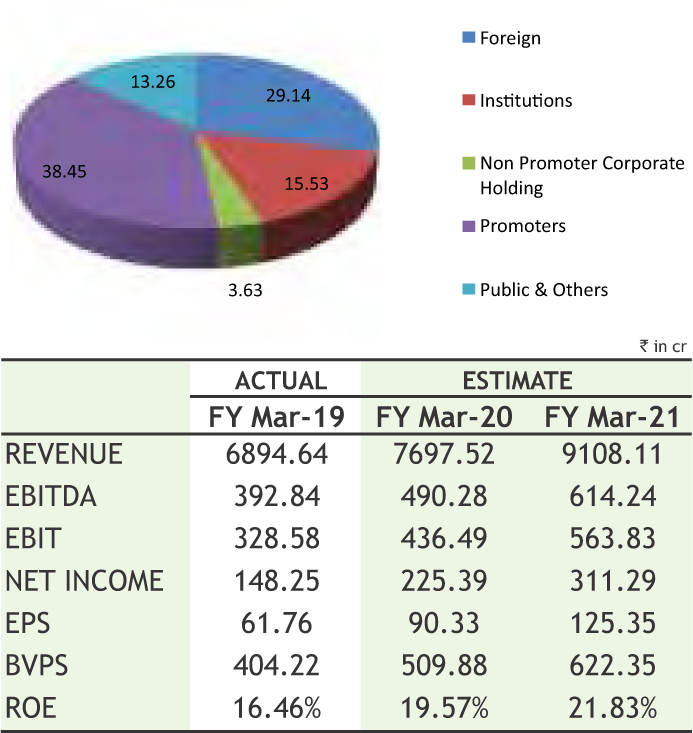

APL Apollo Tubes Limited

CMP: 1560.45

Target Price: 2006

Upside: 29%

| Face Value (Rs.) | 10.00 |

| 52 Week High/Low | 1682.65/1009.05 |

| M.Cap (Rs. in Cr.) | 3784.15 |

| EPS (Rs.) | 76.77 |

| P/E Ratio (times) | 20.33 |

| P/B Ratio (times) | 3.12 |

| Dividend Yield (%) | 0.88 |

| Stock Exchange | BSE |

Investment Rationale

• APL Apollo Tubes (APAT) is the largest producer of Electric Resistance Welded (ERW) Steel Pipes and Sections in India with a manufacturing capacity of 2.55 mn MTPA. It has always been a pioneer in new technologies & an innovative product which has helped it grow faster than its peers. It also invests continuously in enhancing brand awareness and develops the brand which in turn is creating entry barriers for new entrants.

• According to the management, operating environment is getting better and it would report stronger Ebitda per tonne from Q3FY20 onwards.

• During the September quarter 2019, it has reported sales volume grew by 20% to 3.63 lakh tonne in Q2FY20 from 3.04 lakh tonne in Q2FY19 led by structural pipes among others despite external challenges such as, muted demand sentiments in the domestic market, slowdown in construction activity and flooding in key markets like Karnataka, Kerala and Maharashtra.

• Moreover during this quarter, it has also included the impact of full operations of Apollo Tricoat and management expects healthy volumes from Apollo Tricoat would further assist overall volume growth in coming quarters.

• On the development front, APAT recently concluded the acquisition of a production unit located at Hyderabad owned by Taurus Value Steel and Pipes (subsidiary of Shankara Building Products) in the month of May for Rs 70 crore. Commercial production began in the month of June. The acquisition has added production capacity of 200,000 MTPA which includes black pipes (45,000 MTPA), GI pipes (30,000 MTPA) and GP pipes (125,000 MTPA). The capacity is currently operating at a monthly run rate of 10,000 tons and will gradually be ramped up to a peak of 15,000 TPM over the next two years. GP and GI pipe capacities will be operational by December-19.

• The company had planned capex of Rs 200 crore in FY20 which is already completed and a maintenance capex of Rs 20 is expected for H2FY20. Interest cost is expected to go below Rs 50 crore in H2FY20.

• Net revenues increased 11% to Rs. 3,728 crore in H1FY20 compared to Rs. 3,367 crore in H1FY19. EBITDA was higher by 6% Y-o-Y to Rs. 206 crore. PBT stood at Rs. 107 crore as compared to Rs. 112 crore. Net Profit after Tax was at Rs. 112 crore compared to Rs. 74 crore

Risk

• Challenges in steel sector

• Commodity prices

Valuation

The company is doing well and management of the company expects steel demand in India is expected to grow around 6-8% by FY21, of which, steel pipe will form 10-12% of the total steel demand and proportion indicates the significant opportunity for steel pipe consumption in the years to come. The company remains confident of delivering a sales volume growth of 20% CAGR in FY20 & FY21.Thus, it is expected that the stock will see a price target of Rs.2006 in 8 to 10 months time frame on an expected P/Ex16 and FY21 (EPS) of Rs.125.35.

Source: Company Website Reuters Capitaline

Above calls are recommended with a time horizon of 8 to 10 months.

6

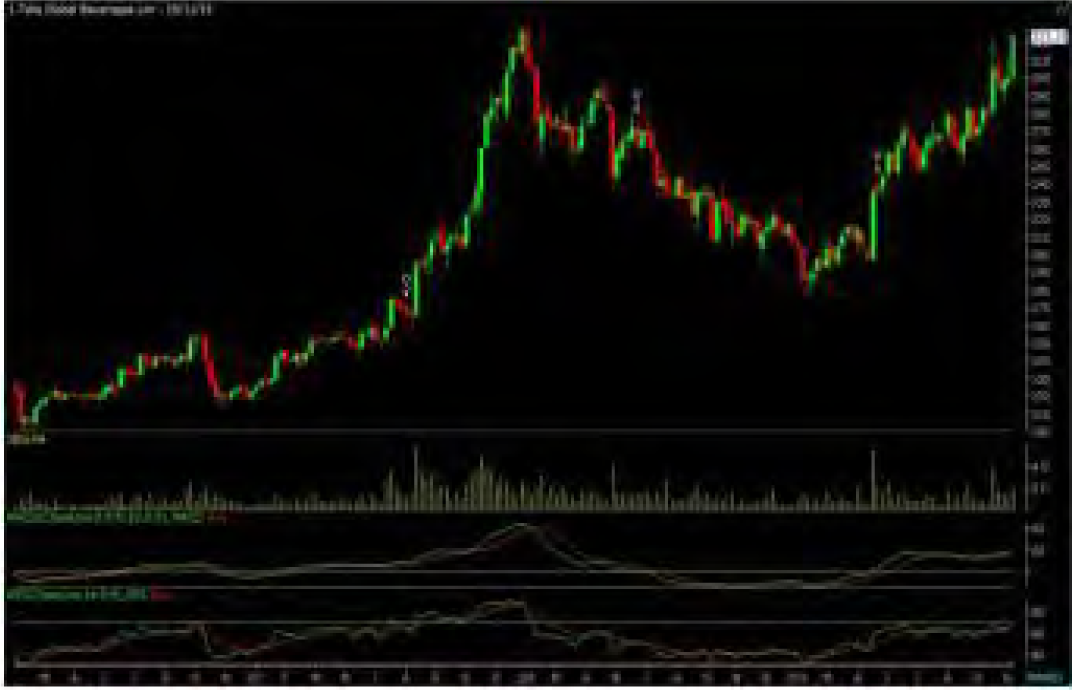

The stock closed at Rs 926.25 on 29th November, 2019. It made a 52-week low of Rs 682 on 04th September 2019 and a 52-week high of Rs. 1024 on 29th March 2019. The 200 days Exponential Moving Average (DEMA) of the stock on the daily chart is currently at Rs 833.57

After sharp correction from 1400 levels, the stock has found support around 700 and spent 6-7 week in narrow range and formed rounding bottom on weekly charts, started moving higher. Last week, it has formed a long bullish candle and also has managed to close near week’s high. So, follow up buying can expect in coming days. Therefore, one can buy in the range of 900-910 levels for the upside target of 980-1000 levels with SL below 860.

The stock closed at Rs 323.15 on 29th November, 2019. It made a 52-week low at Rs 177.05 on 11th February 2019 and a 52-week high of Rs. 324.90 on 29th November 2019. The 200 days Exponential Moving Average (DEMA) of the stock on the daily chart is currently at Rs 259.07

As we can see on charts that stock is trading in higher highs and higher lows on weekly charts, which is bullish in nature. Last week, the stock has formed a long Marubozu candlestick along with high volumes which shows market participants are much bullish for the stock. Therefore, one can buy in the range of 315-318 levels for the upside target of 345-350 levels with SL below 298.

Disclaimer : The analyst and its affiliates companies make no representation or warranty in relation to the accuracy, completeness or reliability of the information contained in its research. The analysis contained in the analyst research is based on numerous assumptions. Different assumptions could result in materially different results.

The analyst not any of its affiliated companies not any of their, members, directors, employees or agents accepts any liability for any loss or damage arising out of the use of all or any part of the analysis research.

SOURCE: CAPITAL LINE

Charts by Spider Software India Ltd

Above calls are recommended with a time horizon of 1-2 months

7

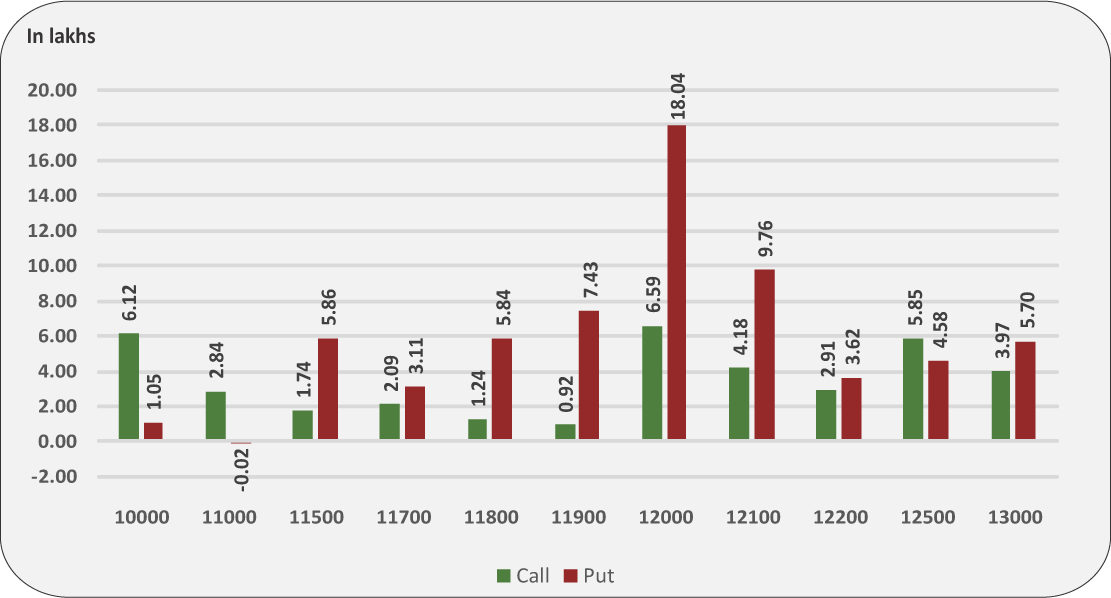

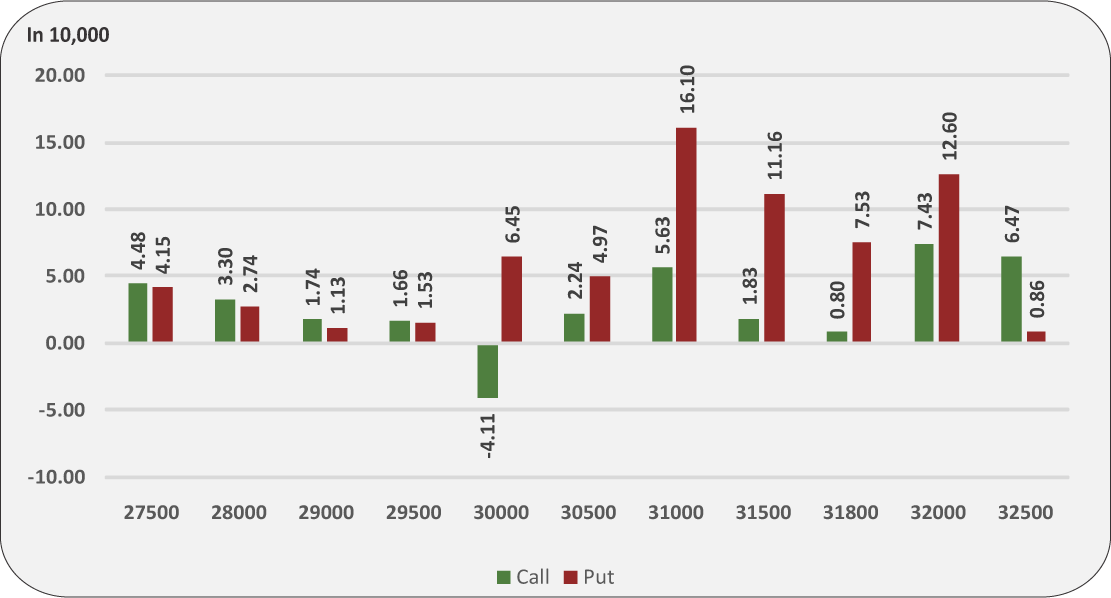

After testing record highs in November series, Nifty indices begin December series with negative note as traders lock profits at higher levels. However, on weekly basis both the indices nifty and banknifty ended on a positive note with gains of more than 1% and 2.5% respectively. On derivative front, call writers were seen adding open interest at 12100 strikes, which may act as crucial hurdle for the index moving forward. On the downside, 12000 & 11950 should act as immediate support levels. From technical front, Indian markets currently maintaining their uptrend and seen trading in a rising channel with formation of higher highs and higher lows on daily and weekly charts. However, secondary oscillators suggest that we might witness some consolidation at higher levels after last week sharp upside. Never the less some stock specific action would remain on radar with sector specific moves. The Implied Volatility (IV) of calls closed at 12.19% while that for put options closed at 13.15%. The Nifty VIX for the week closed at 13.99% and is expected to remain volatile. PCR OI for the week closed at 1.27. For coming week, we expect that the consolidation in index at higher levels is likely to happen in coming sessions, and any dip into the prices should be use to create fresh longs as broader trend is still intact in favor of bulls. On a higher side 12100 in Nifty can act as immediate resistance level and any decisive move above that should trigger follow up buying which can Nifty towards new record highs.

8

|

|

|

|

**The highest call open interest acts as resistance and highest put open interest acts as support.

# Price rise with rise in open interest suggests long buildup | Price fall with rise in open interest suggests short buildup

# Price fall with fall in open interest suggests long unwinding | Price rise with fall in open interest suggests short covering

9

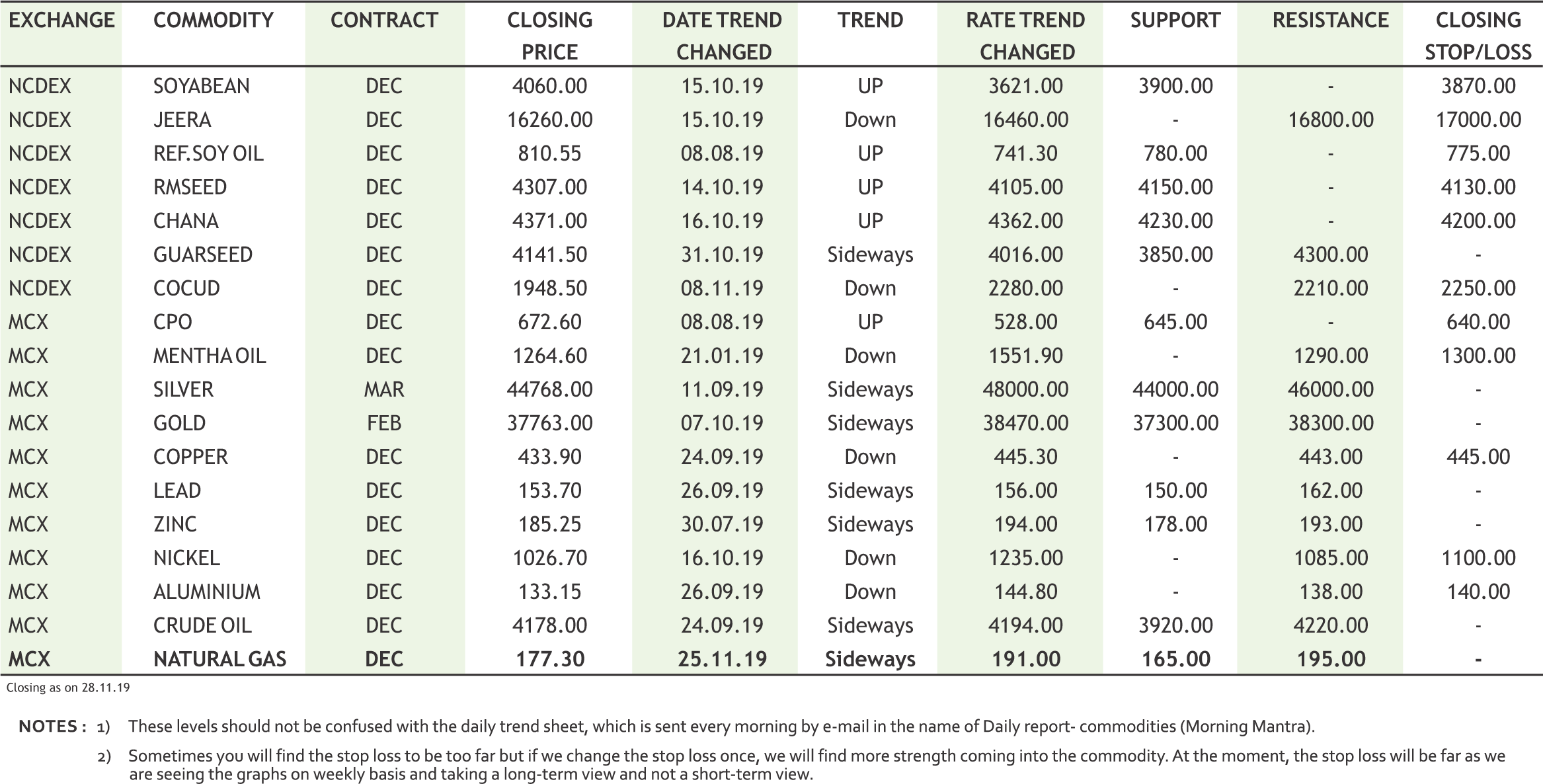

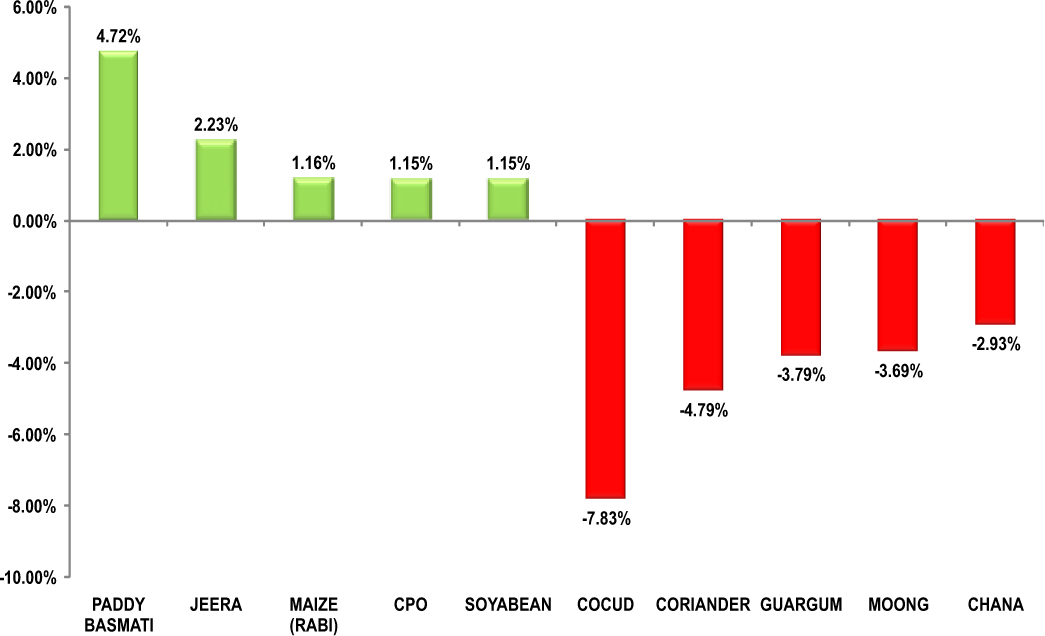

Turmeric futures (Dec) is hovering near its yearly low of 5560 & this bearish trend is likely to get extended towards 5400 levels, due to weak fundamentals of excess poor quality supplies on the spot markets against subdued demand. It is reported that the turmeric farmers are not getting remunerative price as the traders are not coming forward to purchase turmeric citing low quality. The producers are not even being able to preserve their turmeric produce in godowns because the quality of produce would start declining further as worms begin to eat it. On the spot markets these days, only medium and poor quality turmeric are arriving for sale. Jeera futures (Dec) is expected to consolidate & trade with an upside bias in the range of 15800-16700 levels. The factor of slower pace of sowing in the ongoing 2019-20 (Oct-Sep) season may add gains to the counter. The acreage in Gujarat, was at 59,710 ha as on Nov 25, compared with 1,22,249 ha in the corresponding period last year, data from the state farm department showed. Dhaniya futures (Dec) may trade sideways to down in the range of 6500-6900 levels. The sowing has picked up in Gujarat, and sluggish demand will also weigh on the prices. Coriander acreage in Gujarat, the second-largest producer, was at 9,623 ha as on Nov 25, compared with 7,602 ha in the corresponding period last year, data from the state farm department showed. Cardamom futures (Dec) is expected to trade with an upside bias in the range of 2750-3000 levels. The farmers have almost harvested their last round of stocks in the season and this will have an effect on arrivals.

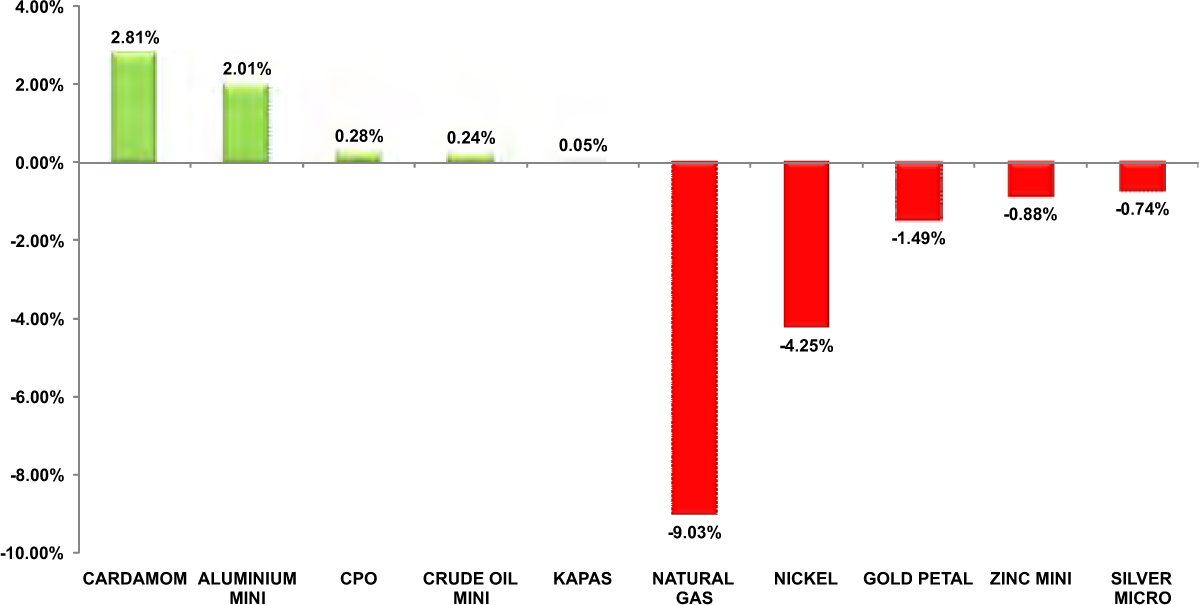

Bullion counter may trade with mixed bias as uncertainty regarding initial trade deal between US and China and geopolitical tensions to keep investors jittery. Gold may trade in a wider range of 37500-38200 whereas on the other hand silver may recover towards 45000 while taking support near 43800. December being a crucial month we will be getting more clarity on the tentative meeting that will be held between US and China and UK elections that is scheduled on 12th December. Also boosting risk appetite was robust U.S. economic data, which assured investors of the health of the country's economy and bringing justice to the Fed Governor positive statements. U.S. economic growth picked up slightly in the third quarter and weekly jobless claims also declined, while core capital goods ordered posted their biggest gain in nine months. U.S. President Donald Trump last week signed into law congressional legislation backing protesters in Hong Kong, prompting Beijing to warn of “firm counter measures”. Gold, considered a safe store of value during economic or political uncertainties, has gained more than 13% this year, mainly due to the tariff dispute. Recently Fed governor Powell mentioned that monetary policy is in a good place which indicates that there is no possibility of a rate cut in the last policy meeting for this year scheduled this month in December. Gold holdings with SDPR ETF, the world's biggest gold-backed fund, were steady at 896.47 tonnes. Gold has been stuck in the $1450-1480/ounce and may continue in this range unless we get more clarity on US-China trade issue and Fed’s monetary policy.

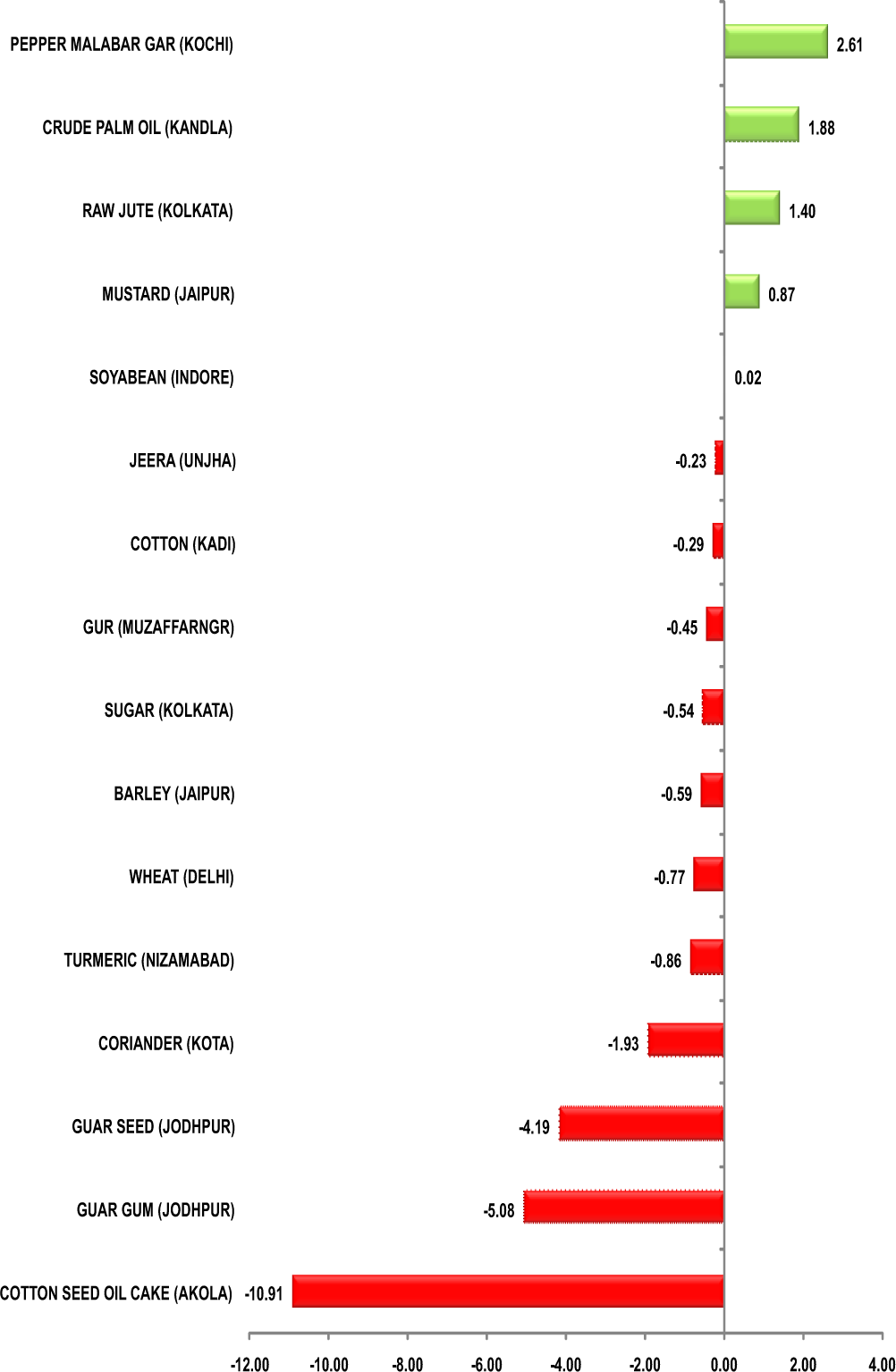

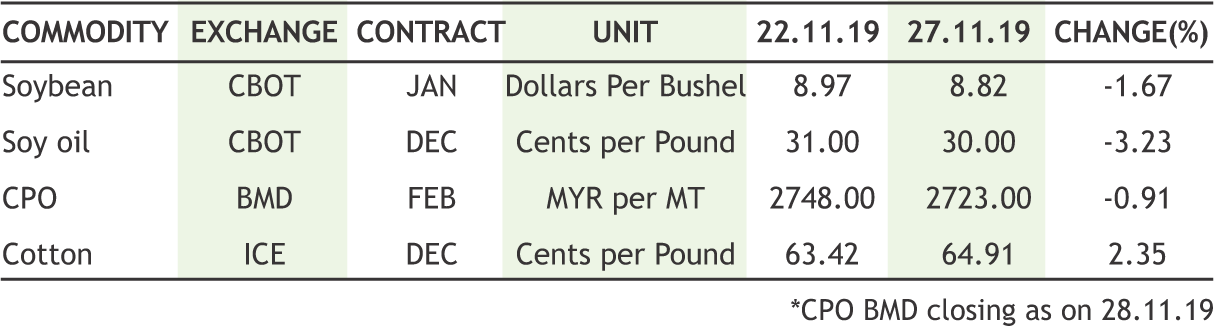

Soybean futures (Dec) may continue to face resistance near 4120-4150 levels as the demand side is weak. It is being estimated that India’s soyameal exports for the oil year 2019-20, starting October, may see a sharp decline at 10 lakh tonnes, a sharp decline from the previous year’s 21.79 lakh tonnes. Indian soyameal is expensive in the world market. In addition to a lower crop, the lack of clarity in continuation of the incentive under the MEIS scheme is hurting export order bookings. Mustard futures (Dec) will possibly trade sideways to up in the range of 4250-4370 levels. The market participants are cautious & closely watching the sowing progress in the major growing regions. This season sowing has been delayed & the latest statistic show that all India as on 22nd November 50.71 lakh hectares has been sown as compared to 53.62 lakh hectares. The deficit in sowing in seen increasing week on week based on the data finding that it was -2.11% during mid of this month, but now it is widened to -5.43%. CPO futures (Dec) would probably make a new life time high on the national bourse as it has the potential to test 680-690 levels. While, soy oil futures (Dec) is also expected to trade on a bullish note towards 825-830, if crosses the previous high of 818.20 levels. There are talks in the market that the government is considering putting restrictions on the import of all kinds of refined edible oils while continuing to keep crude oils under the free category. The need to amend the existing trade policy has arisen as the duty on both crude and refined palm oil is going to be lowered from January 1, 2020.

Crude oil prices may remain on sideways path as participants have now shifted their focus on this week’s meeting on 5th and 6th December OPEC and allies including Russia, a group known as OPEC+, which have been withholding production to support prices. It is expected that OPEC+ to roll over its current production-cut deal, which is set to expire at the end of March, by three to six months. Meanwhile Russian oil companies proposed not to change their output quotas as part of the global deal until the end of March, putting pressure on OPEC+ to avoid any major policy change. They also offered to exclude production of gas condensate, light oil, from the output quotas as Russia has been struggling to meet its supply-reduction targets in recent months. Easing supply concerns, Libya's National Oil Corp said facilities at the 70,000-bpd El Feel oilfield had suffered only minor damage in fighting over the past two days, allowing production to restart. On MCX, Crude oil may trade with mixed path as it can take support at 4100 while facing resistance near 4300. The downside pressure can persist in natural gas counter as prices can dip lower towards 170 while facing resistance near 195. Not only are the weather patterns changing in US but the country is also split with winter storms on the western United States and milder temperatures elsewhere. Earlier the weather models were supportive with rising expectations for a cold December but now the models shifted to milder before trending warmer.

Cotton futures (Dec) may witness short covering towards 19500-19700. The cotton prices are ruling firm at major markets in Maharashtra and Karnataka, while remained steady in Gujarat, Madhya Pradesh and Andhra Pradesh supported by procurement by Government agency. The Cotton Corporation of India (CCI) has purchased 1.2 million bales or about one per cent of total cotton arrivals in the ongoing season that started in October. In the international market, ICE cotton futures may trade sideways in the range of 64-66 cents per pound. The investors are waiting for further developments on trade negotiations between the United States and China. The United States and China are close to agreement on the first phase of a trade deal, U.S. President Donald Trump said, after top negotiators from the two countries spoke by telephone and agreed to keep working on remaining issues. Expect prices to stay range bound, but could see a spike on a trade deal announcement. Chana futures (Dec) may witness correction towards 4300- 4265 levels. The consumer affairs ministry has recommended removal of quantitative restrictions on import of pulses to preempt any price rise because of low production. Also, it is reported that the government is likely to extend the deadline for importing tur to Dec 31. Over the last few months, the government has received several representations for extension of the date of import of pulses. Guar seed futures (Dec) may trade with a downside bias in the range of 4000-4190, while guar gum futures (Dec) may break 7400 & plunge further towards 7200 levels. The arrivals are expected to catch pace from the non-irrigated belts of Barmer, Jaisalmer, etc.

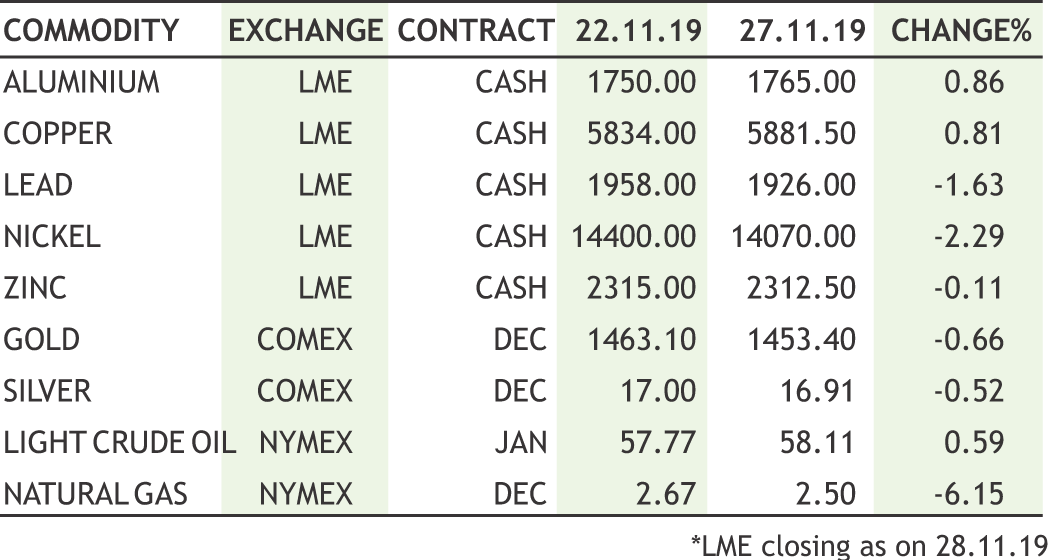

Base metal counter may trade with subdued path. PMI numbers from China and US due this week are likely to show activity shrank for a seventh consecutive month in November. However, profits at China’s industrial firms shrank at their fastest pace in eight months in October. Copper may trade sideways to downside bias and it can test 425 levels while taking resistance near 445 levels. Combined copper inventories in LME and ShFE warehouses, at around 350,000 tonnes, are at typical levels for this time of year. But stockpiles in Chinese bonded warehouses, at 243,800 tonnes, are down from near 400,000 tonnes a year ago and the lowest since at least 2013. Meanwhile, lead may remain sideways as it can move in the range of 150-158 levels. Zinc may remain subdued as it can test 180 levels while facing resistance near 192 levels. Nickel prices can move with weaker path and may dip lower towards 1000 levels while taking resistance near 1080 levels. Nickel has come under pressure from worries about demand from stainless steel mills, mostly located in China, which account for roughly two thirds of consumption estimated at about 2.4 million tonnes this year. Historically low inventories of nickel, at less than 70,000 tonnes, and high cancelled warrants at nearly 34% are expected to support prices. Aluminium prices can further witness bounce back as It can 138 levels while taking support 128 levels. Aluminium has been gaining strength as the Cash-3M spread stood at $US11 a tonne, around highs of the year.

10

|

COPPER MCX (DEC) contract closed at Rs. 433.90 on 28th Nov’19. The contract made its high of Rs. 452.30 on 14th Oct’19 and a low of Rs.432.05 on 26th Nov’19. The 18-day Exponential Moving Average of the commodity is currently at Rs. 436.67.On the daily chart, the commodity has Relative Strength Index (14-day) value of 37.05.

One can sell around Rs. 438 for a target of Rs.425 with the stop loss of Rs. 445.

CRUDE OIL MCX (DEC) contract closed at Rs. 4178 on 28th Nov’19. The contract made its high of Rs. 4222 on 22nd Nov’19 and a low of Rs. 3696 on 3rd Oct’19. The 18-day Exponential Moving Average of the commodity is currently at Rs. 4104.06 On the daily chart, the commodity has Relative Strength Index (14-day) value of 58.07.

One can buy above Rs.4220 for a target of Rs. 4500 with the stop loss of Rs. 4100.

JEERA NCDEX (DEC)contract was closed at Rs. 16260 on 29th Nov’19. The contract made its high of Rs. 17155 on 04th Nov’19 and a low of Rs. 15840 on 15th Nov’19. The 18- day Exponential Moving Average of the commodity is currently at Rs. 16277 on the daily chart, the commodity has Relative Strength Index (14-day) value of 48.98.

One can sell at Rs. 16600 for a target of Rs. 15500 with the stop loss of Rs 17100.

11

• The PMO has asked agriculture and food and consumer affairs ministries to start monitoring price sensitive crops right from the sowing stage for timely price interventions.

• The CCEA has accorded its approval for mandatory packaging of foodgrains and sugar in jute material for 2019-20.

• The government has procured 305,420 tn coarse cereals so far in 2019-20 (Oct-Sep), compared with 181,450 tn in the year ago period.

• NCDEX has revised the Tick size and Lot Size of COTTON SEED OIL CAKE, GUARSEED, SOYABEAN & SOY OIL with effect from December 02, 2019 in all the running contracts and yet to be launched futures contracts.

• The Jeera contract scheduled to expire on December 20, 2019 shall now expire on December 13, 2019. Further, the tender period shall now commence from, December 09, 2019.

• The Cotton Advisory Board estimated India's 2019-20 (Oct-Sep) cotton production to rise by 9.1% to 36 mln bales (1 bale = 170 kg) due to an increase in acreage this year,

• China has just given the long-awaited green light to the trading of new commodity options including iron ore and rapeseed.

• China has brought forward 1 trillion yuan ($142 billion) of the 2020 local government special bonds quota to this year as it seeks to avert a sharper economic slowdown.

• Profits of China's industrial firms fell 9.9% in October from a year earlier to 427.56 billion yuan ($60.74 billion), compared with a 5.3% decline in September.

In the week gone by, bullion counter remained in tight range on mixed fundamentals. Market participants are taking cues from the US President’s comments on the trade deal being close to signing quite sincerely but at the same time an uptick in the dollar is weighing on the precious metal pack. US President’s latest signing of congressional legislation backing protesters in Hong Kong has made Beijing unhappy. Chinese officials also commented that this is their internal matter and no third party interference is required on the same and market participants are hoping no further delay will happen due to this added friction between US and China. Gold took support near 37500 while silver took support near 43800-44000. Base metals after a brief rally witnesses some profit taking as uncertainty between US and China on trade war kept the metals pack volatile. Copper dipped lower below 430 levels on uncertainty regarding US trade deal. US legislation requires the State Department to certify that Hong Kong retains enough autonomy to justify favourable US trading terms that have helped it to maintain its position as a world financial centre. It doesn't look as if anything is going to be agreed any time soon. Nickel also traded lower and broke the key level of 1050. While Natural gas fell sharply lower as it went below 180 on the back of forecasts for warmer-than-normal temperatures in U.S. Crude oil traded sideways path. Crude oil remained under pressure as the official data showed that US crude and gasoline stocks rose and President Donald Trump signed into law a bill backing protesters in Hong Kong, fuelling tensions with China. Crude stockpiles in the United States swelled by 1.6 million barrels as production rose to a record 12.9 million barrels per day (bpd) and refinery runs slowed, the Energy Information Administration stated.

Cardamom prices held steady thanks to active demand from exporters in gulf countries. The exhaustion of stock following the end of the season in Guatemala has forced overseas buyers to look at Indian variety to meet their requirements. While, jeera also bounced back from its lows as the sowing pace has slowed down in major growing regions. The oilseeds counters maintained an upside bias owing to market talks that the Government is thinking to restrict the edible oil imports. While, coriander prices plunged as the sowing increase in the major producing areas. Chana also witnessed weakness due to dull demand from millers amid lesser consumption of its by-products.

|

|

12

|

|

Gold has been a currency for thousands of years. There are no mentions of the dollar, euro, yen, pound, or any of the other currencies in any manuscript or historical sculpture, but gold and silver are prominently featured.

Gold is the ultimate hard currency. Gold is a ‘must have’ financial asset indeed’. Not only investors, but also nation’s central banks try to hoard gold in times of crisis as gold is playing a new role in the changing international financial environment.

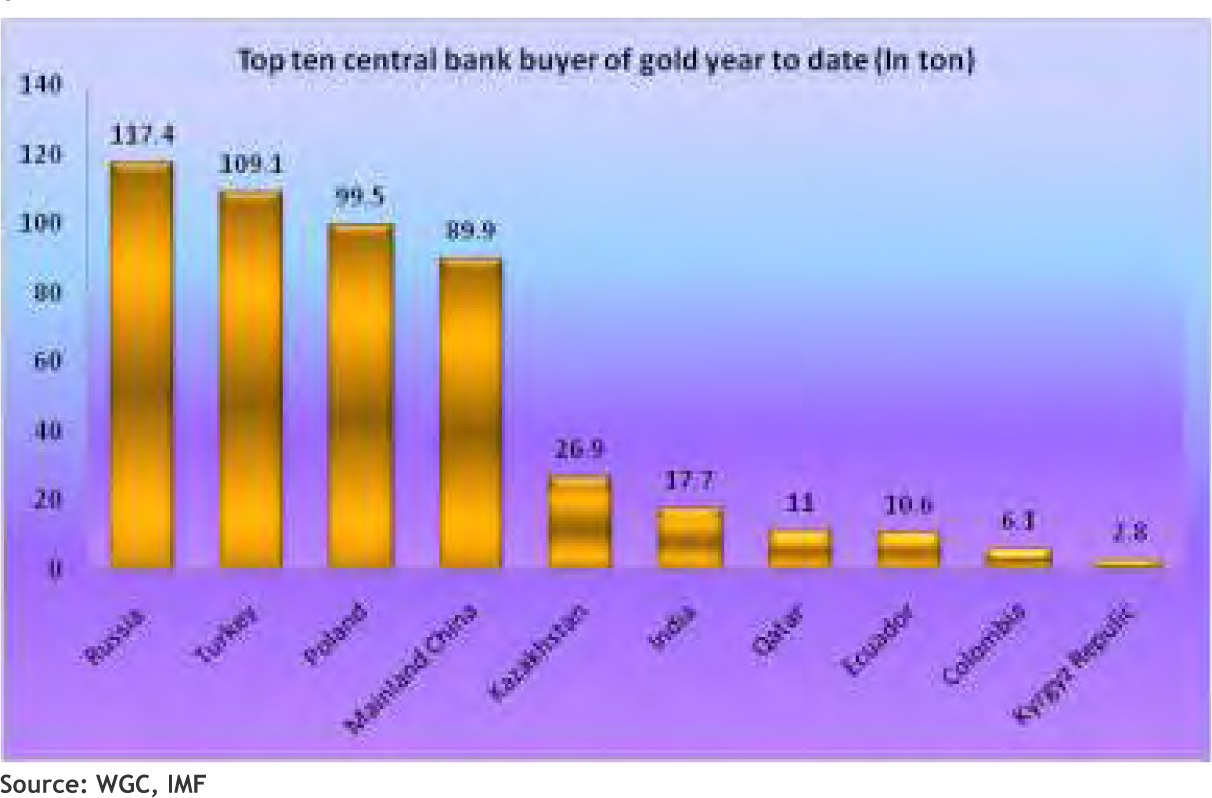

Love affair of global central banks with gold is amazing

Central banks across the world are aggressively adding gold to their foreign exchange (forex) reserves. According to data from the World Gold Council (WGC), the net gold purchases by central banks was 651.5 tons in 2018, the highest level of annual net central bank gold purchases since the suspension of dollar convertibility into gold in 1971. Notably, the centralbanks buying have also become geographically more diverse as several new countries adding gold for the first time in decades.

In 2019, the big players have been Russia, Turkey, and Poland

• According to the World Gold Council, a dozen central banks increased their gold holdings by at least one ton through the first eight months of 2019.

• Russia and China have been the leading buyers despite of significant gold producers. Russia added another 11.3 tons to its hoard in August and increased its gold holdings by 117.4 tons this year alone. The Russian Central Bank's gold reserves topped $100 billion in September.

• China bought another 5.9 tons in August, the ninth straight month of gold purchases for the People's Bank of China and increased its gold holdings by nearly 90 tons this year.

• The January to June period saw the highest levels of central bank purchases since 2010. Poland was the top buyer, with reserves growing 77 percent to 100 tonnes.

• Qatar increased its gold reserves by 11 tons in 2019.

• In August, two central banks sold gold amounts greater than one ton. Kazakhstan shrunk reserves by 2.6 tons. This was a reverse in course. The Kazakh central bank has been aggressively buying gold.

• Uzbekistan sold another 2.2 tons of gold in August after dumping 22.4 tons in July.

Why Central-Bank Gold Buying Picked Up

• Gold is a 100 percent guarantee from legal and geopolitical risks. Preserving its historical value, gold continues to be one of the safest assets in the world.

• The gold enhance the long-term stability of countries reserves and strengthen market confidence even under normal market circumstances.

• A report from the Dutch central bank “If the entire system collapses, the gold stock provides a collateral to start over. Gold gives confidence in the power of the central bank’s balance sheet. That gives a safe feeling.”

• Considering the uncertainty like volatility or a correction in the stock market as well as dollar, central bankers are adding gold to their reserves as a hedge as they don’t want to be caught unawares like they were in 2008

• Some Countries want to reduce the amount of U.S. dollar from its forex reserve portfolio and just looking for ways to diversify of reserves as they desire to move from dollar dependent global financial system to multi-polar reserve system. In the case of Russia, officials simply want to move away from the U.S. dollar. Russia has recently sold the majority of its holdings of U.S. Treasuries, and the Bank of Russia said it will continue the policy of de-dollarization.

13

|

| 26th NOV | Powell says FED is ‘strongly committed’ to 2% inflation goal. |

| 27th NOV | Growth down, but no fear of recession: Finance Minister. |

| 28th NOV | Trump signs Hong Kong democracy legislation. |

| 28th NOV | China signals hope for trade deal despite US Law supporting Hong Kong. |

| 28th NOV | Government wants RBI to buy out stressed assets of shadow banks. |

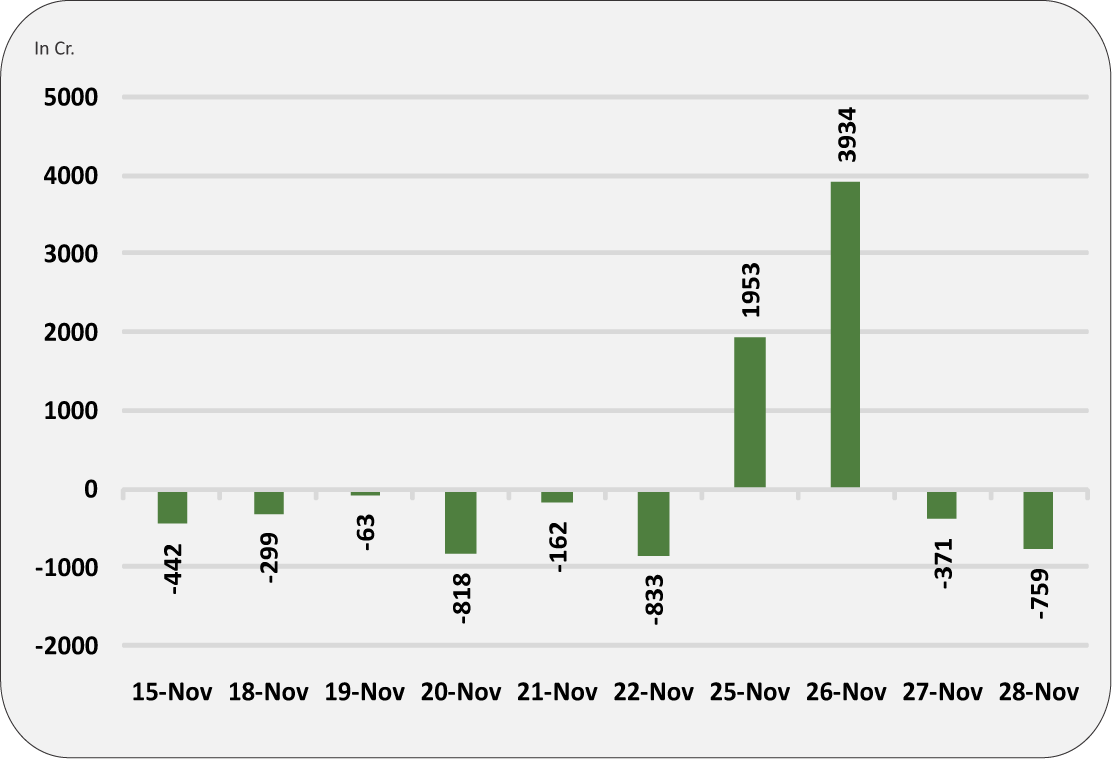

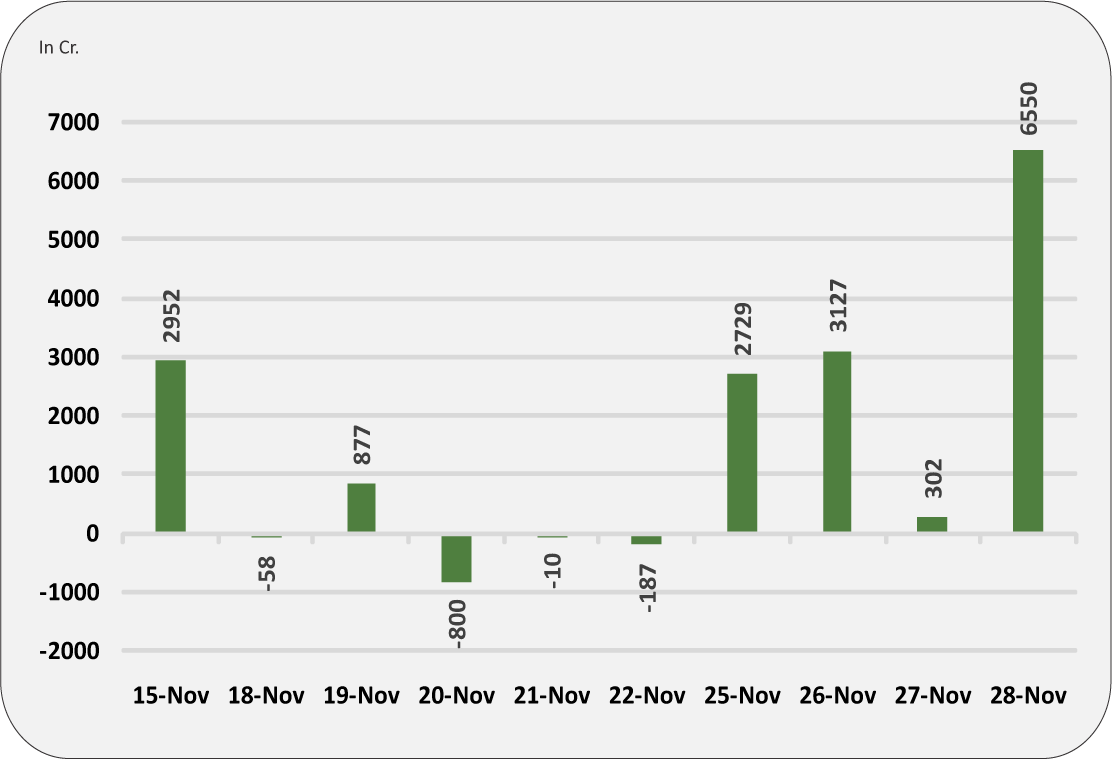

Global capital flows across emerging markets including India capped the on-going weakness in domestic currency this week. Due to convergence of global monetary policy and improved risk-on sentiment in trade war, it is inevitable to say that despite weak fundamental in emerging economies, foreign Investors have poured more than Rs 14,500 crore in November in India which is an eight months high reversing the turmoil faced in August this year. Although Rupee remains the worst performing currency in EM FX pack amid regular intervention from RBI to accumulate dollars. Meanwhile Trump support for Hong Kong pro democracy group is the only risk factor for risk-on mode as Chinese government may turn-off from phase one deal. Progressively Donald Trump has signed two US bills supporting Hong Kong’s pro-democracy protesters, defying calls from China to block the legislation and putting the territory’s special trade status at risk. The president ratified the Hong Kong Human Rights and Democracy Act after it was overwhelmingly passed by Republican and Democrat lawmakers, a rare example of bipartisan co-operation mandates, US executive branch annually re-examine Hong Kong’s status and imposes sanctions on anyone who has suppressed human rights in the former British colony. Going forward next week, rupee move will be guided from the expectation of RBI policy.

USDINR is likely to stay above 71.30 and move higher towards 72.10 in the next week.

|

USD/INR (DEC) contract closed at 71.8025 on 28th Nov’19. The contract made its high of 71.9525 on 25th Nov’19 and a low of 71.4075 on 28th Nov’19 (Weekly Basis). The 14-day Exponential Moving Average of the USD/INR is currently at 71.80.

On the daily chart, the USD/INR has Relative Strength Index (14-day) value of 50.75. One can buy at 71.70 for the target of 72.30 with the stop loss of 71.40.

EUR/INR (DEC) contract closed at 79.1550 on 28th Nov’19. The contract made its high of 79.4825 on 25th Nov’19 and a low of 78.7675 on 28th Nov’19 (Weekly Basis). The 14-day Exponential Moving Average of the EUR/INR is currently at 79.42.

On the daily chart, EUR/INR has Relative Strength Index (14-day) value of 43.33. One can sell at 79.55 for a target of 78.95 with the stop loss of 79.85.

GBP/INR (DEC) contract closed at 92.8650 on 28th Nov’19. The contract made its high of 92.9325 on 28th Nov’19 and a low of 91.89 on 27th Nov’19 (Weekly Basis). The 14-day Exponential Moving Average of the GBP/INR is currently at 92.56.

On the daily chart, GBP/INR has Relative Strength Index (14-day) value of 58.18. One can buy at 92.55 for a target of 93.15 with the stop loss of 92.25.

JPY/INR (DEC) contract closed at 65.7150 on 28th Nov’19. The contract made its high of 66.29 on 25th Nov’19 and a low of 65.36 on 28th Nov’19 (Weekly Basis). The 14-day Exponential Moving Average of the JPY/INR is currently at 66.09.

On the daily chart, JPY/INR has Relative Strength Index (14-day) value of 39.87. One can buy at 65.70 for a target of 66.30 with the stop loss of 65.40.

14

| Industry | Banking |

| Total Issue (Shares) - Fresh Issue | 202,702,703 |

| Net Offer to the Public | 202,702,703 |

| Issue Size (Rs. Cr.) | 750-729 |

| Price Band (Rs.) | 36-37 |

| UFSL's shareholder reservation | 10% size of the issue |

| UFSL's shareholder price discount | Rs.2 of price Band |

| Offer Date | 2-Dec-19 |

| Close Date | 4-Dec-19 |

| Face Value | 10 |

| Lot Size | 400 Shares |

| Total Issue for Sale | 202,702,703 |

| QIB | 152,027,027 |

| NIB | 30,405,405 |

| Retail | 20,270,270 |

1. Augmenting the Bank's Tier - 1 capital base to meet our Bank's future capital requirements 2. Meeting the expenses in relation to the Issue 3. Receive the benefits of listing the Equity Shares on the Stock Exchanges |

| Book Running Lead Manager | Kotak Mahindra Capital Company Ltd IIFL Securities Limited JM Financial Limited |

| Name of the registrar | Karvy Fintech Private Limited |

Considering the P/BVx valuation on the upper end of the price band of Rs. 37, the stock is priced at P/B ratio of 2.77x on the pre issue book value of Rs.13.37 and on the post issue book value of Rs.17.23 , the P/B comes out to 2.15x.

On the lower end of the price band of Rs.36 the stock is priced at P/B ratio of 2.69x on the pre issue book value of Rs. 13.37 and on the post issue book value of Rs. 17.23, the P/B comes out to 2.09x.

About the company:

Ujjivan Small Finance Bank Limited (USFB), incorporated in 2017, offers small finance to underserved & unserved segments in India. On October 7, 2015, UFSL received RBI In-Principle Approval to establish an SFB, following which it incorporated Ujjivan Small Finance Bank Limited as a wholly-owned subsidiary. UFSL offers small size loan products to economically poor women, individual loans to Micro and Small Enterprises (MSEs). Among the leading SFBs in India, the Bank had the most diversified portfolio, spread across 24 states and union territories as of March 31, 2019.

Strength

Pan-India presence: As of September 30, 2019 the company was present in 24 states and union territories encompassing 232 districts in India. As of September 30, 2019, it operated from 552 Banking Outlets that included 141 Banking Outlets in URCs (of which seven were business correspondent centres) and additionally operated four Asset Centres. Its diversified operations also allow it to de-risk its business by mitigating political and state-specific risks. As of September 30, 2019, it operated 131, 167, 173 and 81 Banking Outlets (including in URCs) in the North, South, East and West regions, respectively.

Diversified portfolio offering:USFB launched “Sampoorna Banking” in April 2019. USFB's portfolio of products and services includes various asset and liability products and services. Its asset products comprise: (i) loans to micro banking customers that include group loans and individual loans, (ii) agriculture and allied loans, (iii) MSE loans, (iv) affordable housing loans, (v) financial institutions group loans, (vi) personal loans, and (vii) vehicle loans.

Customer centric organization with multiple delivery channels: As of September 30, 2019, USFB served 4.94 million customers and operated from 552 Banking Outlets that included 141 Banking Outlets in Unbanked Rural Centres ("URCs") (of which seven were business correspondent centres) and additionally operated four Asset Centres. In Fiscal 2019 alone, it operationalized 287 Banking Outlets. As of September 30, 2019, it had a network of 441 ATMs that accept RuPay, Visa and MasterCard. As of September 30, 2019, its two 24/7 phone banking units based in Bengaluru and Pune service customers in 11 languages while its mobile banking application is accessible in five languages.

Strong track record of financial performance: Its Net Interest Income in Fiscal 2018 and 2019 was Rs 861Cr and Rs 1106.4 Cr, respectively, and was Rs 740.42 Cr in the six months ended September 30, 2019. Its Net Interest Margins (NIM) in Fiscal 2018 and 2019 were 10.31% and 10.93%, respectively, and was 10.64% in the six months ended September 30, 2019. Total deposits have increased from Rs 206.40 Cr as of March 31, 2017 to Rs 7379.44 Cr as of March 31, 2019 and were Rs 10129.85 Cr as of September 30, 2019. Of its total deposits, its share of retail deposits has increased from 3.15% as of March 31, 2017 to 37.07% as of March 31, 2019 and was 41.93% in the six months ended September 30, 2019. Moreover, its CASA to total deposits ratio has improved from 1.57% as of March 31, 2017 to 10.63% as of March 31, 2019 and was 11.87% as of September 30, 2019.

Strategy

Diversify product offerings to enable multiple customer relationships: As per the company its endeavour is to be a one-stop-shop for financial services, delivering quality products and solutions, along with a personalized customer experience to a diversified customer base.

Continue to focus on technology and data analytics to grow operations: The optimum use of

advanced, cost-effective technology has significantly driven its operations, and going forward, it

intends to strategically invest its resources for further integration of technology into its operations.

Strengthen liability franchise and focus on increasing its retail base: It believes that with simple,

flexible products, which are accessible through assisted and self-serviced channels, it can position

itself as a reliable alternative to informal players.

Diversify its revenue streams: As per the RHP, an important strategic focus for the company is to diversify fee and non-fund based revenues. It intends to leverage on its Banking Outlet network, digital channels and its increasingly diversified product and service portfolio to develop its fee and commission-based business.

Risk Factor

• Limited operating history

• Rely on information technology

• Subject to stringent regulatory requirements and prudential norms

• Banking industry is very competitive.

Outlook

Ujjivan Small Finance Bank Limited is a mass market focused Small Finance Bank in India. It has established a diversified portfolio, spread across 24 states and union territories as of 31 March 2019. Meanwhile, the total gross advances is 12863.65 Crore, out of which almost 80% of the advances are unsecured, which is under the category of micro lending. Taking into account its growth prospects, the issue price is attractively valued. A long term investor may opt the issue.

15

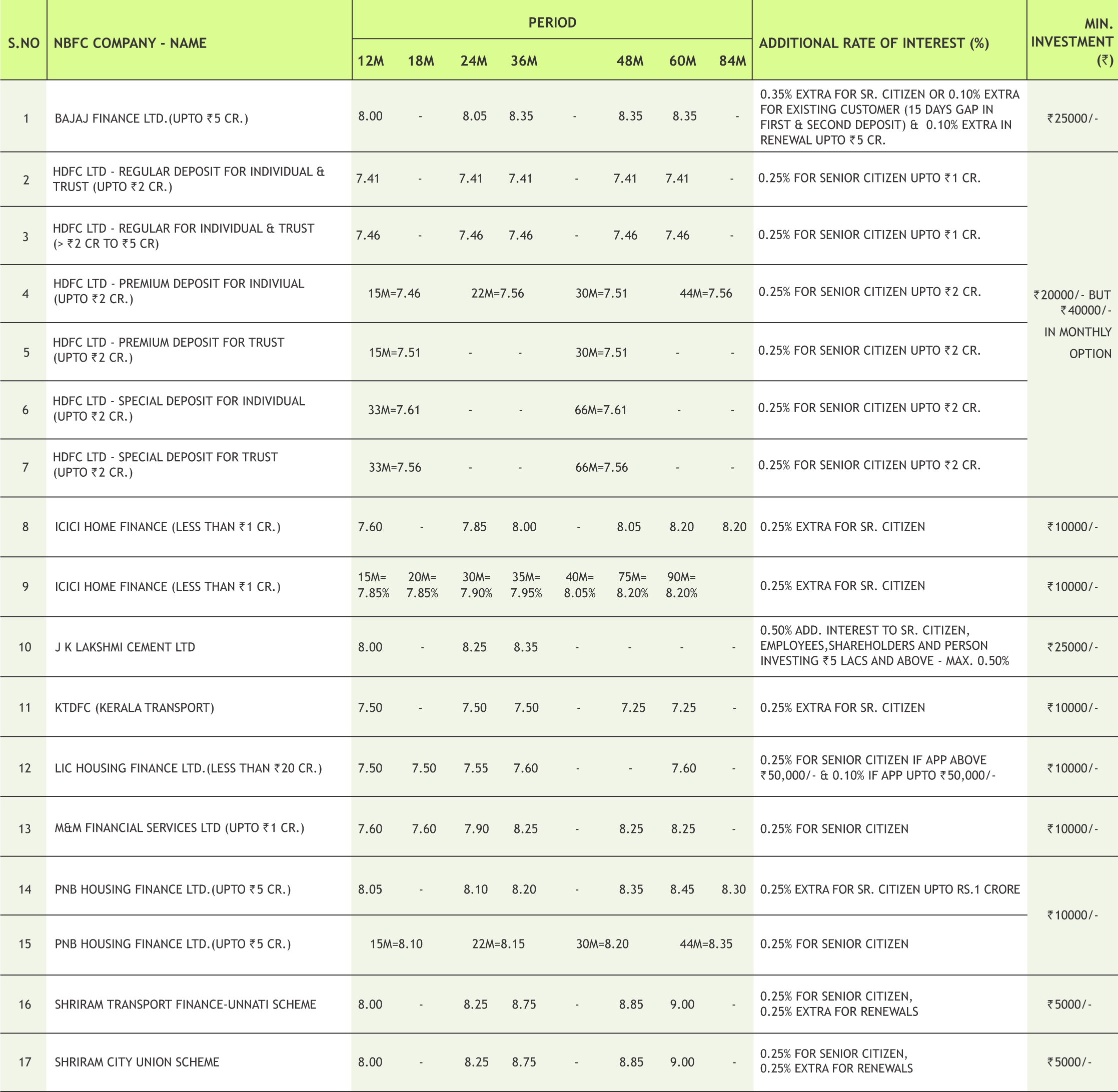

|

* Interest Rate may be revised by company from time to time. Please confirm Interest rates before submitting the application.

* For Application of Rs.50 Lac & above, Contact to Head Office.

* Email us at fd@smcindiaonline.com

16

|

|

|

|

|

Note:Indicative corpus are including Growth & Dividend option . The above mentioned data is on the basis of 08/08/2019 Beta, Sharpe and Standard Deviation are calculated on the basis of period: 1 year, frequency: Weekly Friday, RF: 7%

*Mutual Fund investments are subject to market risks, read all scheme related documents carefully

18

Mr. S C Aggarwal (CMD, SMC Group), Mr. Mahesh C Gupta (Vice CMD, SMC Group) & other Key Directors along with SMC Employees celebrating the milestone of achieving 10,000 SIPs in BSE Star MF held on Thursday 28th November, 2019 at Delhi & Mumbai offices.

Mr. Ajay Garg (Director & CEO, SMC Group) & Mr. Nitin Murarka (Head - Research) during an Investor Awareness Seminar organized in association with NSE, HDFC Mutual Fund & NSDL held on Tuesday 26th November, 2019 at Hotel Platinum Inn, Ahmedabad.

REGISTERED OFFICES:

11 / 6B, Shanti Chamber, Pusa Road, New Delhi 110005. Tel: 91-11-30111000, Fax: 91-11-25754365

MUMBAI OFFICE:

Lotus Corporate Park, A Wing 401 / 402 , 4th Floor , Graham Firth Steel Compound, Off Western Express Highway, Jay Coach Signal, Goreagon (East) Mumbai - 400063

Tel: 91-22-67341600, Fax: 91-22-67341697

KOLKATA OFFICE:

18, Rabindra Sarani, Poddar Court, Gate No-4,5th Floor, Kolkata-700001 Tel.: 033 6612 7000/033 4058 7000, Fax: 033 6612 7004/033 4058 7004

AHMEDABAD OFFICE :

10/A, 4th Floor, Kalapurnam Building, Near Municipal Market, C G Road, Ahmedabad-380009, Gujarat

Tel : 91-79-26424801 - 05, 40049801 - 03

CHENNAI OFFICE:

Salzburg Square, Flat No.1, III rd Floor, Door No.107, Harrington Road, Chetpet, Chennai - 600031.

Tel: 044-39109100, Fax -044- 39109111

SECUNDERABAD OFFICE:

315, 4th Floor Above CMR Exclusive, BhuvanaTower, S D Road, Secunderabad, Telangana-500003

Tel : 040-30031007/8/9

DUBAI OFFICE:

2404, 1 Lake Plaza Tower, Cluster T, Jumeriah Lake Towers, PO Box 117210, Dubai, UAE

Tel: 97145139780 Fax : 97145139781

Email ID : pankaj@smccomex.com

smcdmcc@gmail.com

Printed and Published on behalf of

Mr. Saurabh Jain @ Publication Address

11/6B, Shanti Chamber, Pusa Road, New Delhi-110005

Website: www.smcindiaonline.com

Investor Grievance : igc@smcindiaonline.com

Printed at: S&S MARKETING

102, Mahavirji Complex LSC-3, Rishabh Vihar, New Delhi - 110092 (India) Ph.: +91-11- 43035012, 43035014, Email: ss@sandsmarketing.in